Take a Flight to Quality

Actively screening for excellence is today’s keystone for building an emerging markets portfolio.

SubscribeInvesting in emerging markets has traditionally been associated with investing in hot growth themes and geographies. Just think of China’s consumer internet boom, Taiwan’s semi-conductors or India’s fintech revolution. Go back further and the birth of the Asian Tigers comes to mind – those markets whose rapid industrialization provided investors with a potentially ultra-high growth allocation in their portfolios.

In today’s emerging markets, things are different. The enormous potential for growth remains but the focus is less on uncorking geysers of growth and more about seeking exposure to companies across all sorts of markets that are embedded for growth over the long term. Screening for quality in emerging markets has become a paramount requirement.

An easy way to get exposure to emerging markets has been through passive investing, whereby strategies track the particular constituents of an index according to that benchmark’s methodology. It’s become a popular approach, particularly through passive exchange traded funds (ETFs) which can offer greater tax efficiencies and transparency than mutual funds. But while passive investing can capture growth during periods of market stability and economic expansion, it’s more of a challenge in turbulent or down markets. Without an active portfolio manager at the helm, passive strategies don’t have the capability to search out new companies or markets and can be swept into market backwaters away from faster-flowing channels.

Tale of two markets

A textbook illustration of this has been the contrasting fortunes of Taiwan and Vietnam this year. Taiwan, a key global supplier of semiconductors and a common constituent of emerging market benchmarks, has been hurt by softening demand in the chip industry, while Vietnam, a lower profile, frontier market, has experienced rapid industrial growth. Active funds have been able to counter the challenges of other markets by leveraging the strength of Vietnam, something passive funds have been powerless to do.

But investing in today’s emerging markets is not simply about looking for strong geographies and economies. It’s about looking for strong, emerging companies. That means businesses that exhibit strong balance sheets and cash flow, have good, sustainable ownership structures and good relations with stakeholders, like regulators, creditors and employees. Emerging markets have come a long way since their budding in the latter half of the 20th century. To progress and grow in this century they need to embrace some of the attributes of Western companies—like stability and oversight—and this is particularly important in today’s uncertain times.

Right now, emerging markets aren’t so much characterized by distinct themes as they are impacted by macro headwinds, like inflation and rising interest rates, a strong U.S. dollar and China’s COVID policy. Investing in quality companies is the strongest foundation possible for enduring these headwinds, in our view. Growth stocks without profits or cash, and legacy companies with entrenched cost structures and dried-up moats are likely to wither.

Actively managing emerging-markets exposure and screening for quality means hard examination of companies and their suppliers and engaging with the management of businesses. The Matthews Emerging Markets Equity Fund, Matthews Asia Innovators Fund and Matthews China Fund—which are also available as active ETFS (MEM, MINV, MCH, respectively)—all do this.

Inseparable from screening for quality is identifying the potential for businesses to deliver outperformance over the long term. Emerging markets still offer an enormous canvas for growth. In fact, many companies in these markets have become, or are on the verge of becoming, key players in industries of the future, like renewable energy and transportation, robotics and artificial intelligence. A lot of the upstream materials and energy that are required for renewable industries, for example, are located within emerging market economies.

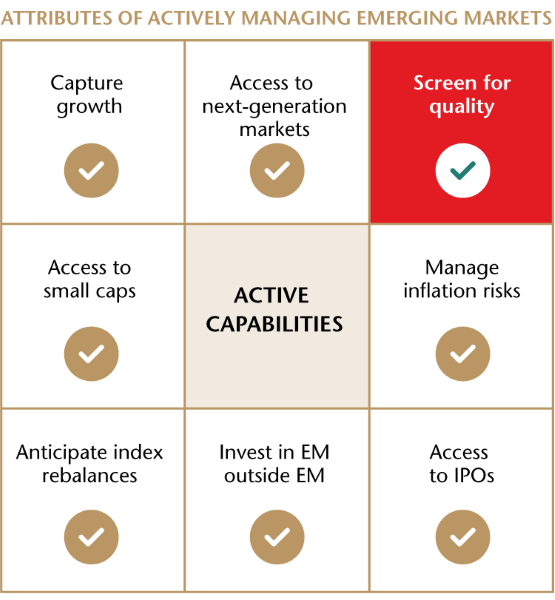

There are many attributes of actively managed investing, including the ability to find and capture growth, to investing in Western companies with large emerging markets exposures, to accessing companies initially listing on public markets, to diversifying into new markets and asset classes like small caps. But the key trait of the moment is the capability to maximize visibility and screen for quality in order to build strong platforms for future growth. Down the road, investors may find these long-term quality plays become the new sought-after companies, industries and geographies of emerging markets.

Definitions:

Cash flow: The amount of cash and cash equivalents that come in and go out of a company. Cash received represents an inflow and cash spent represents an outflow.

DISCLOSURES

You should carefully consider the investment objectives, risks, charges and expenses of the Matthews Asia Funds before making an investment decision. A prospectus or summary prospectus with this and other information about the Funds may be obtained by visiting matthewsasia.com. Please read the prospectus carefully before investing as it explains the risks associated with investing in international and emerging markets.

The value of an investment in the Fund can go down as well as up and possible loss of principal is a risk of investing. Investments in international, emerging and frontier markets involve risks such as economic, social and political instability, market illiquidity, currency fluctuations, high levels of volatility, and limited regulation. Additionally, investing in emerging and frontier securities involves greater risks than investing in securities of developed markets, as issuers in these countries generally disclose less financial and other information publicly or restrict access to certain information from review by non-domestic authorities. Emerging and frontier markets tend to have less stringent and less uniform accounting, auditing and financial reporting standards, limited regulatory or governmental oversight, and limited investor protection or rights to take action against issuers, resulting in potential material risks to investors. Investing in small- and mid-size companies is more risky than investing in larger companies as they may be more volatile and less liquid than large companies. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Pandemics and other public health emergencies can result in market volatility and disruption.