Completing Your China Exposure: Small Companies Help Capture China's New Growth Drivers

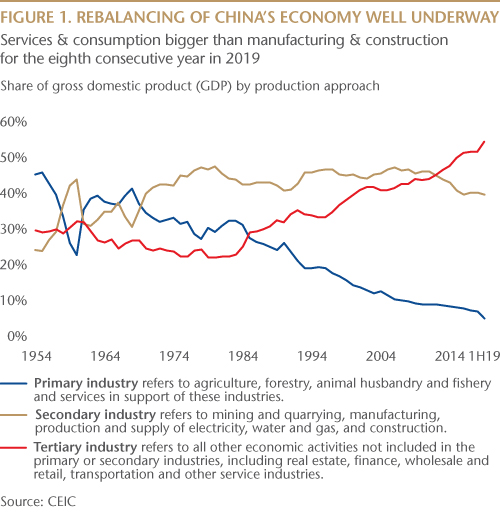

As China's economy continues its shift toward services and consumption, small and medium-sized businesses are accelerating this transformation.

As China's economy continues its shift toward services and consumption, small- and medium-size businesses are accelerating this transformation. China's entrepreneurs are introducing new business paradigms, disrupting old ways of doing business and laying the groundwork for outsize growth opportunities. For investors seeking alpha, China's small caps may present a compelling opportunity. We believe low research coverage in the market leaves the field open for finding undiscovered companies with untapped growth potential. Furthermore, the domestic focus of small companies can provide an element of protection against trade tensions and other geopolitical macro risks.

Many investors today may already have exposure to China via investment strategies tilted toward larger companies. For investors specifically looking to access China's dynamic growth potential, adding exposure to small companies can help complete a China allocation. China's small caps can help improve diversification by providing access to a universe of companies with little to no overlap with most developed or emerging markets (EM) benchmarks. With attractive Sharpe ratios relative to emerging markets, China's small caps can help improve the broader risk/reward profile of an overall portfolio. Additionally, China's small caps have historically been less risky than many investors may expect—volatility for China's small caps is similar to U.S. small caps, and have historically been less volatile than China's large caps over the long run.

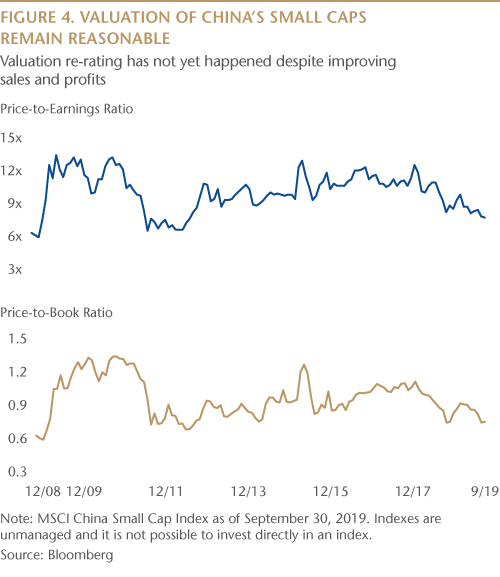

Valuations for China's small companies remain near the lower end of their historical range, which we find an appealing entry point for investors who believe in the long-term secular growth potential of China. We expect the gap between small and large companies to narrow over time as investors take a closer look at the quality and growth trajectories of China's small companies. Quality metrics of many small caps, including high return on equity, are positive and many companies generate a solid return on their assets, together with attractive earnings-per-share growth opportunities. Finding the top-quality companies in the universe of China's small caps requires an active approach, however, as not all small companies are value creators. Here are some of the reasons we believe that China's small companies deserve a closer look.

Entrepreneurs Drive China's New Economy

Small-cap companies in China are at the forefront of the country's economic shift away from fixed asset investments such as manufacturing, infrastructure and real estate, and toward innovation, consumption and services. China's smaller companies tapping into the entrepreneurial spirit across cities and provinces tend to thrive mostly in productivity- and value-enhancing industries such as automation, health care, e-commerce and education. These areas are under-represented in large cap-oriented benchmarks and portfolios. Small-cap companies have the entrepreneurial spirit and flexibility to recognize and respond to changing local market trends, including changing patterns of consumption. We believe China's transition to entrepreneur-driven growth could lead to value creation and attractive investment opportunities among small caps.

Vast Universe of Small Companies Offers Differentiated Exposures

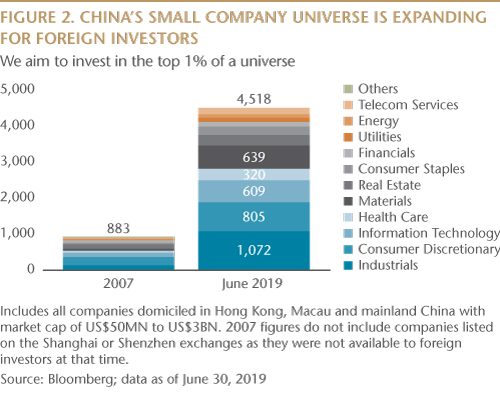

China's small-cap equity universe has expanded exponentially over the past decade to become the largest small-cap market in the world. Surpassing the U.S., there are more small companies listed, and higher average daily liquidity, in China's accessible small-cap market than in the U.S. China provides a broad investment universe for stock pickers: approximately 4,500 companies with a market capitalization of less than US$3 billion, which we define to be small cap, are domiciled in China. By way of comparison, China's largest companies can be several hundred billion and up in market capitalization. Because many of China's small companies remain relatively unknown, active managers can uncover high-quality companies with good corporate governance at attractive valuations.

Alpha Opportunities Are Substantial

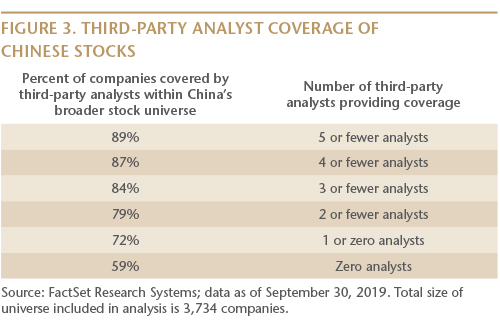

The broad universe of Chinese equities is widely uncovered by sell-side analysts. Of 3,700 Chinese equities for which FactSet Research Systems tracks analyst coverage, most companies (89%) are covered by five or fewer analysts and more than half (59%) are not covered at all by third-party, sell-side research providers. Many of these companies reside in the small-cap universe. This information asymmetry creates an advantage for fundamental active managers.

Small Caps Appear Poised to Re-Rate on Strong Earnings Growth and Low Valuations

Over a recent five-year period, from 2014 to 2018, China's large caps as a group have outperformed their small cap counterparts. Investment styles tend to rotate over longer periods, however, and we believe there is an opportunity for small companies to perform well versus their larger peers over the coming years—particularly given attractive valuations and strong earnings growth. We expect China's small-cap universe to be considered as an investment asset class over time and for small-cap stocks to perform in line with their strong earnings growth profile.

While the supply of new companies available to invest in has expanded, demand from foreign investors has been slow to develop over the past five years ended September 2019. This mismatch of supply and demand of China's small-cap stocks has resulted in low valuations and weak overall stock returns during this time. We believe it also creates an opportunity for forward-thinking investors. The composition of China's overall equity markets is changing as foreign institutional investors start to increase their allocations to China.

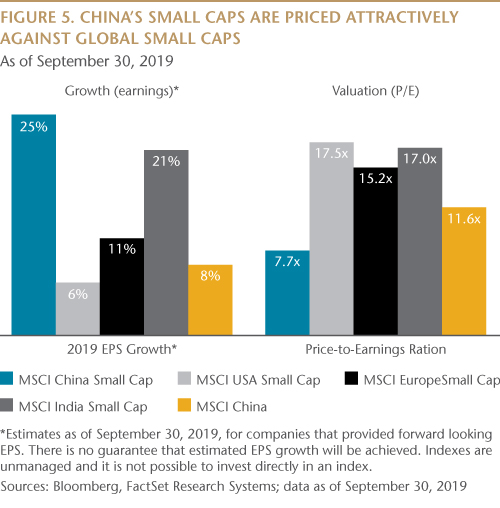

Earnings Growth Has Outpaced Other Small Caps Globally

China's small companies currently have similar earnings growth to small companies in India, and higher earnings growth than U.S. small companies, European small companies and China's large companies. What's more, valuations are low when compared to other small companies globally. Accordingly, we believe valuations have the potential to rise.

Domestic Focus Buffers Trade Risks

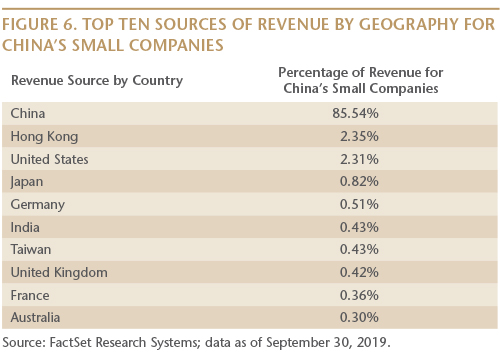

China's small companies have low exposure to U.S. exports, with only 2% of revenues coming from sales to the U.S. In contrast, China's small companies generate roughly 85% of their revenue from within China. As trade conflicts have waxed and waned, China's small companies have been relatively immune from direct impacts from tariffs and other trade barriers because of their domestic focus. Trade tensions may also benefit China's small companies in some cases, as tensions are accelerating the development of new supply chains within China, particularly for strategic industries such as semiconductors. Developing new supply chains takes years, rather than months, and we expect continued progress over the next decade and beyond.

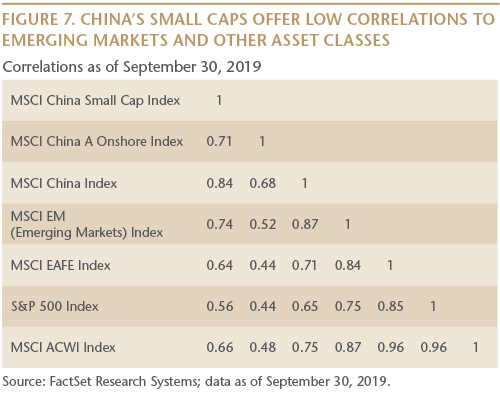

For investors who may be following the trend of deglobalization and its potential impact on emerging markets, it is worth noting that China's small companies have low correlations to broader EM indexes. For investors looking to reduce trade-related investment risks and improve the efficiency of their overall EM portfolios, we believe an allocation to an actively managed strategy focused on China's small companies may provide an additional layer of diversification.

Creating a Well-Rounded China Allocation

At Matthews Asia, we believe that part of an investor's allocation to China should include exposure to companies best positioned to participate in the country's new economy. Because many small companies are still relatively undiscovered, they represent an alpha-rich hunting ground. China's small companies have been historically less volatile over the long run than investors might expect. Accordingly, China's small caps can complement a large-cap allocation to China's equities.

China's economy is among the most entrepreneurial in the world, where change happens fast and disruption is commonplace. Mobile payment systems in China arose from digital platforms, rather than banks. Small companies are going straight to cloud computing, forgoing onsite physical mainframes. A vibrant labor market requires employers to adopt enterprise software to make the most of their human capital, presenting burgeoning software industries with a long runway for growth. We believe capturing these growth opportunities requires dedicated exposure to China's small companies. While the universe for small companies in China is vast, competition is high and only the best-run, most innovative companies are likely to thrive and succeed. Research coverage of China's small companies remains minimal, creating opportunities for active managers conducting proprietary, fundamental research. Earnings growth for China's small companies looks attractive in our view and valuations are low, creating an interesting moment for investors looking to round out their allocation to China.

As investors ask how to tap China's growth potential, we believe the answer lies in aligning investments with the country's underlying growth drivers. A shift toward services requires increased levels of innovation for companies to compete. Rising incomes and domestic consumption requires understanding the tastes and needs of local consumers. Expansion of domestic supply chains for key industries creates opportunities for new businesses to fill gaps in missing goods and services. We believe small companies, as the heart of China's “new economy,” capture China's entrepreneurial spirit, while helping investors meet long-term goals for growth.

Index Definitions

MSCI All Country World Index (ACWI): The MSCI ACWI captures large and mid-cap representation across 23 Developed Markets (DM) and 23 Emerging Markets (EM) countries. With 2,477 constituents, the index covers approximately 85% of the global investable equity opportunity set.

MSCI China A Onshore Index: The MSCI China A Onshore Index captures large and mid-cap representation across China securities listed on the Shanghai and Shenzhen exchanges.

MSCI China Index: The MSCI China Index is a free float—adjusted market capitalization—weighted index of Chinese equities that include China-affiliated corporations and H shares listed on the Hong Kong exchange, and B shares listed on the Shanghai and Shenzhen exchanges.

MSCI China Small Cap Index: The MSCI China Small Cap Index is a free float—adjusted market capitalization—weighted small cap index of the Chinese equity securities markets, including H shares listed on the Hong Kong Exchange, B shares listed on the Shanghai and Shenzhen exchanges, and Hong Kong-listed securities known as Red Chips (issued by entities owned by national or local governments in China) and P Chips (issued by companies controlled by individuals in China and deriving substantial revenues in China).

MSCI Emerging Markets Index: The MSCI Emerging Markets Index captures large- and mid-cap representation across 23 Emerging Markets (EM) countries. With 833 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

S&P 500 Index: The S&P 500 Index is a broad market-weighted index dominated by blue-chip stocks in the U.S.

General Definitions

Correlation: A relationship or connection between two asset classes. A correlation of one (1) indicates a perfect historical correlation between two asset classes. A correlation of less than one (1) indicates lower correlation.

Gross Domestic Product: The total value of goods produced and services provided in a country during one year.

Price-to-Book Ratio (P/B Ratio): Price-to-Book Ratio (P/B Ratio) is used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. A lower P/B ratio could mean that the stock is undervalued.

Price-to-Earnings (P/E) Ratio: Price-to-Earnings Ratio (P/E Ratio) is a valuation ratio of a company's current share price compared to its per-share earnings.